Deltamodel

a structured approach ...

How to calculate a capital weighted stock market index (i.e. DAX®)

The content of this article does not constitute an investment recommendation, but merely serves to provide a basic understanding of information and its contexts. No liability can be accepted for losses incurred on the basis of this article.

Introduction

In this article, I introduce you to the calculation procedures for capital-weighted stock market indices. As an example, Deutsche Börse’s leading index is the Deutsche Aktien Index (DAX®).

The intended audience of the article are all readers who are interested in stock market and finance issues and who want to understand the basis on which the charts are created, which today can be consumed at any time via television, stock market magazines or the Internet.

Previous knowledge is not required for the understanding of the article, you might benefit from having a certain affinity to mathematical methods and models.

Stock market indices

A big advantage of the common stock market indices is that they are within the group of freely available information. This applies even more to todays age of the Internet, where any information that is somehow available can be accessed very quickly and very easily.

On the basis of this freely available information, the calculation of these indices is basically no magic, but without some background knowledge anything but trivial. Exactly this background knowledge I would like to convey to you in sufficient depth with this article.

A market index itself can be understood as a characteristic value which, using a defined calculation method, supplies information on groups and segments of values (stocks) that are likewise defined and can generally be traded on the stock exchange. A stock market index is typically presented as a chronological list of values calculated using this calculation method. This chronological list enables the tracking of the index over a certain period of time, for example in a chart.

Different indexes can have different calculation methods and represent differently defined groups or segments of stocks.

Examples of indices are the DAX ® in Germany as well as the S&P 500 and the Dow Jones in America. The DAX ® represents the 30 largest German enterprises by market capitalization, the Dow Jones and the S&P 500 focus on American companies. These three indices are also a good example of different calculation methods. While the DAX ® is weighted by market capitalization, the Dow Jones weights the price of each stock.

Without spoilering the rest of the article, I would like to warmly recommend that you read the information on the DAX ® published by Deutsche Börse. These include the official information on how the DAX ® is being calculated. This information is published as a so-called “stock index guide” under “(fa fa-external-link) http://dax-indices.com/”: http://dax-indices.com/.

Equally freely available and also highly recommendable are the daily updated key figures published by the stock exchange on the various DAX ® values. These can be downloaded as a table and are suitable for understanding the formulas presented here with practical values.

The German Stock Index DAX ®

The DAX® is a so-called performance index whose individual values are weighted according to market capitalization. The calculation formula of DAX ® is based on the work of the mathematician Étienne Laspeyres and uses values for the prices of the companies at the current calculation date, the closing prices of the considered companies on the trading day before the first inclusion in an index of the stock exchange, the freely available number of shares of the company (both at the current time as well as the time before the company was first included in a Deutsche Börse index) and as a formula for a capital-weighted index also the number of shares that are tradable on the market at all.

This means that it takes into account which shares are in free float (which are the tradable shares) and which shares are fixed to major shareholders and accordingly can not be traded on the stock exchange.

It also takes into account the performance indices characteristic that dividends are paid out and these distributed dividends do not simply disappear from the index calculation but have an impact on the further calculation of the index. In addition, it takes into account the effects of incorporating companies into the index or removing companies from the index.

Calculation of the DAX®

How all these various factors provide impact to the performance of the DAX ® I would now like to illustrate step by step. I also will illustrate these factors are reflected in the calculation formula, in order to give you a sense of how a simplified calculation of an index could actually lead to a market-capital weighted performance index such as the DAX®.

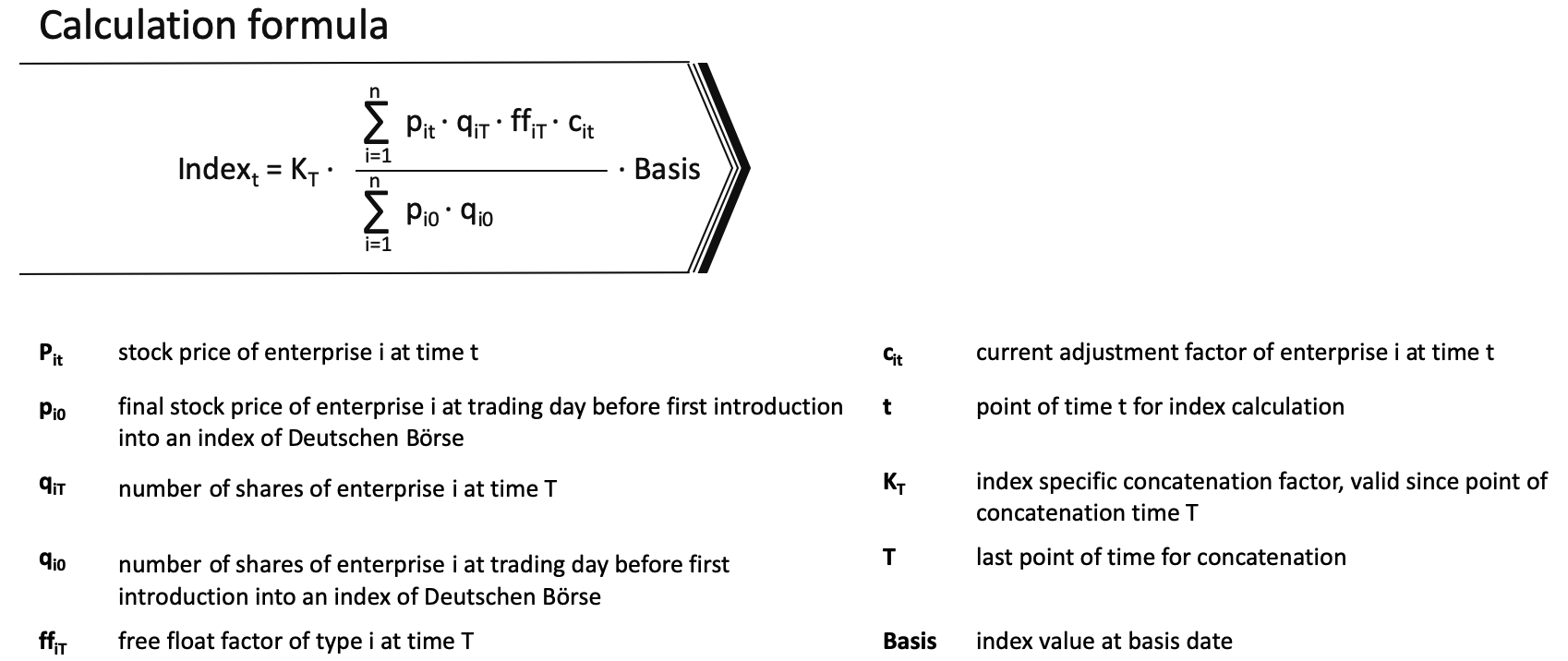

The DAX® is calculated according to the following formula:

In order to give you an understanding how this quite complicated looking formula works, I will break it down and put the chunks together step by step.

Determination of the capital value

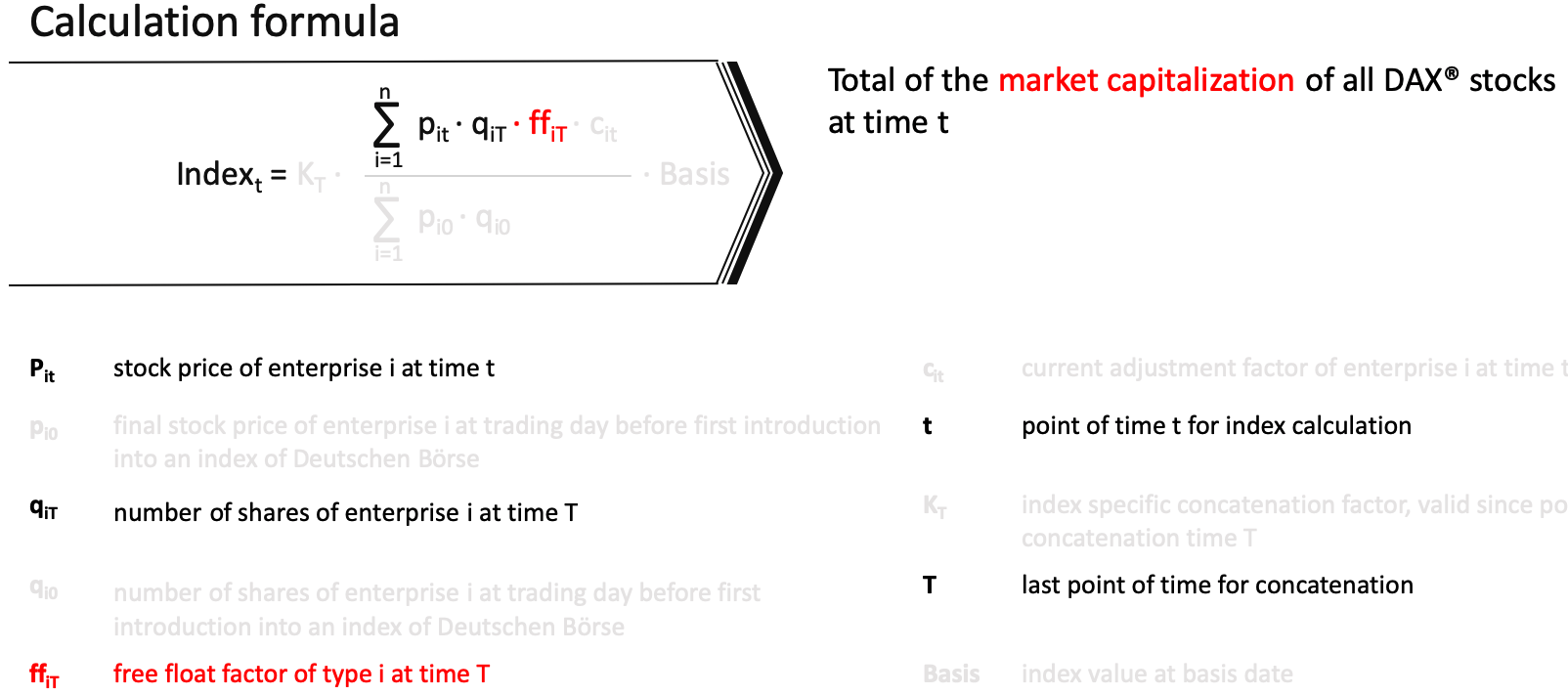

The first step in compounding the formula is to sum up the capital values of all the companies contained in the DAX ®. The capital value of a company is the number of shares in the company multiplied by the respective share price. In order to get comparable results, the share price is calculated from the price at the current time, but the number of shares in the company is not necessarily the number of shares at the current time. The number of company shares relevant to the formula is calculated quarterly at time T in the formula. This time is also referred to as the time of the last so called concatenation. What a concatenation is, will be explained in the section dealing with the concatenation factor.

Determination of the market capitalization

Using the sum of the capital values, the next step is to introduce the so called Free Float Factor. The Free Float Factor is used to convert the capital value into the market capitalization. The difference between capital value and market capitalization is, that the capital value takes into account the total number of shares. The market capitalization takes into account the number of shares which are tradable at an exchange only.

The German stock exchange has published the criteria which determine wether a share package is considered to be tradable or not. With some simplification it can be assumed, that all share packages greater than 5% of the company value are considered to be non-tradable and will have no impact to the calculation of the DAX®. All share packages representing less than 5% of a company value are considered to be tradable and will have impact to the calculation of the DAX®.

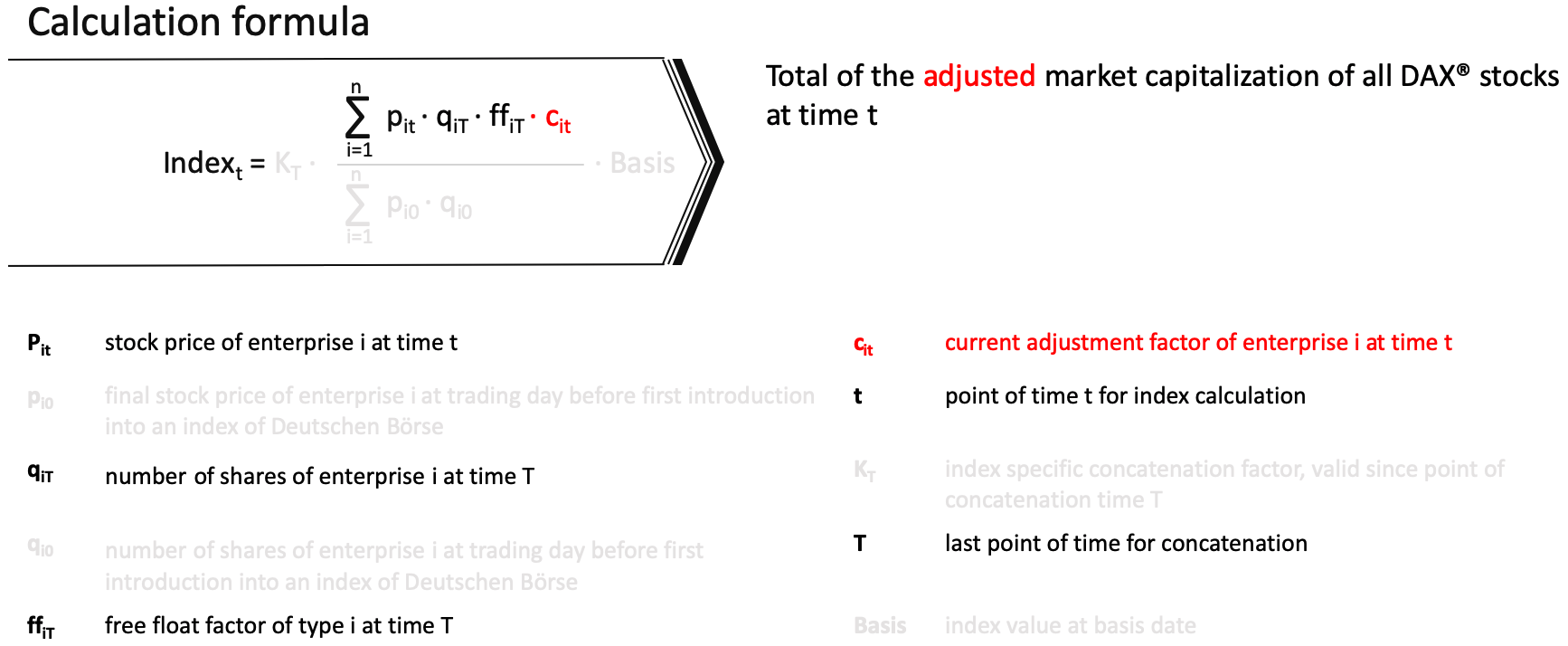

Impact of dividends

Once an enterprise is paying dividends, one can observe that at the dividend payout day the stock price of the enterprise decreases round about the same ratio which the dividends represent in relation to the enterprise value. Since the DAX® is no price index but a performance index the dividends will be included in the DAX® calculation formula.

In order to incorporate the dividends into the calculation formula an adjustment factor for dividends has been introduced. This means, once a company pays dividends the adjustment factor is used to adjust the stock price in a way as if the dividends would have been reinvested. This method prevents price gaps, which would have the biggest impact at times where many companies pay its dividends. For DAX® companies it this most often in late spring and early summer the case. The adjustment factor prevents price gaps caused by dividends.

Introduction of a reference point

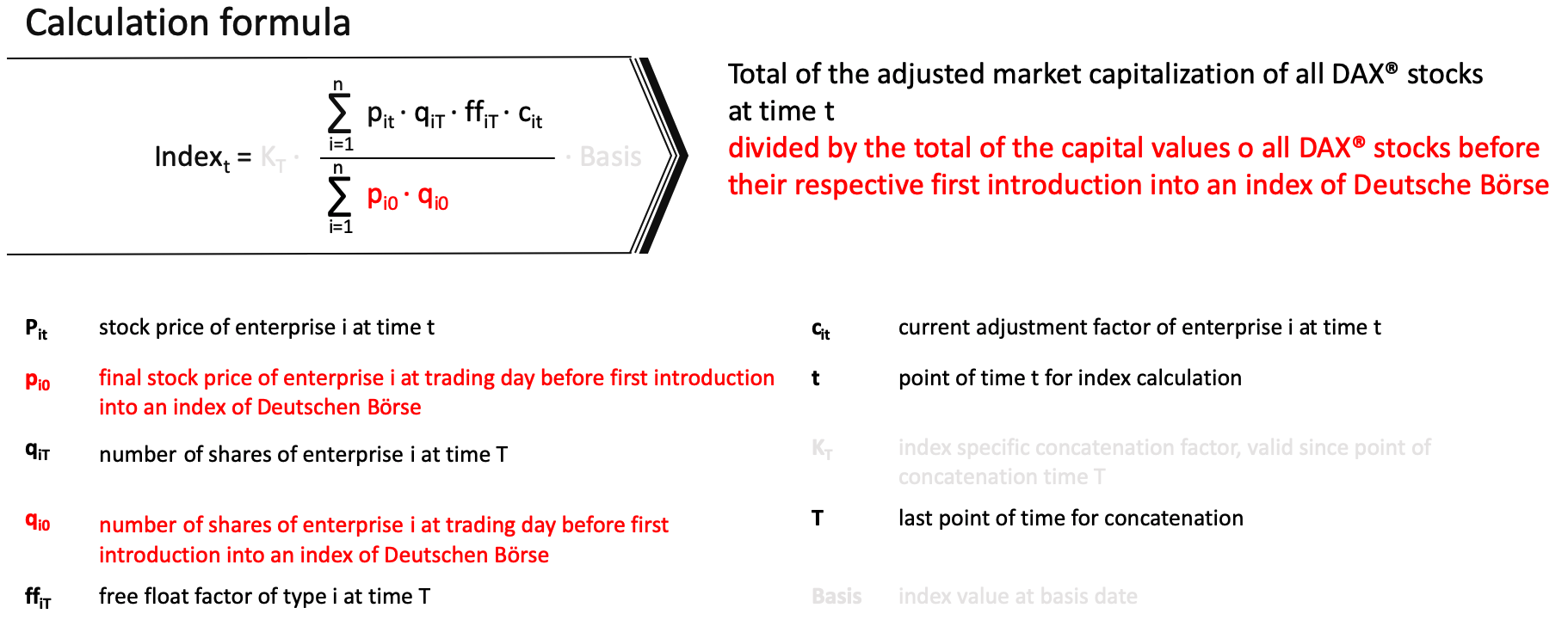

Following the discussion until now enables you to recognize that all factors in the nominator of the formula depend on the current point of time t which makes them somewhat meaningless. What is missing is a reference point which enables comparison of the adjusted market capitalization and an assessment what an increase or decrease of the price really mean. In order to to achieve this kind of assessability the DAX® formula uses the total of all capital values as reference point, using for each stock the value before it was introduced to an Index o Deutsche Börse. This reference point is introduced to the denominator of the formula.

Being aware of, that the DAX® was the first index of Deutsche Börse it can be reproduced easily, that the fraction was 1 at the first day of DAX®. Since the number 1 was not the most attractive base for a stock index it was decided to use 1000 as the base. Consequently the factor Basis is a fixed part of the formula.

Impact of the concatenation factor

A final feature of the formula is the index specific concatenation factor K T. This factor enables to replace companies in the DAX® without changes in the index value. This is important since the index was designed to represent the 30 largest german enterprises. Since new enterprise might grow so much, that they are part of the 30 largest or others decrease, that they are to little for the 30 largest those replacements are performed on a regular basis.

The concatenation factor is used to compensate price changes of the DAX® caused by the replacement of enterprises.

Outlook

This article was written to demonstrate how a capitalization weighted index such as the DAX® is calculated. I hope this article was beneficial to your understanding how such indices are being calculated in general and how it can be done for the DAX® in particular. Maybe you remember the formulas presented when watching the stock market news the next time.